Table of Contents

Compare banks vs fintech apps and avoid hidden transfer fees when sending money from France

Introduction

Sending money from France can be more expensive than most expats expect. Hidden fees, exchange rate markups, and slow bank transfers often reduce the final amount received.

When people move to France, they usually expect a few cultural adjustments. Maybe the paperwork. Maybe the famous French bureaucracy. Maybe the endless requests for documents.

Anyone who has rented an apartment here knows the famous “dossier” stress — proof of address, payslips, tax statements, identity documents, and signatures everywhere.

But what many expats don’t expect is how expensive international money transfers can be.

If you regularly send money from France, understanding these hidden costs is essential.

A friend of mine learned this lesson the hard way when she tried to transfer money internationally.

After moving to France, she needed to send money from her UK account to pay the security deposit on a small apartment. The transfer seemed simple enough:

Euros → Euros

Bank → Bank

Europe → Europe

She was transferring 5000€ from her UK bank account to a new French account to pay the apartment security deposit.

But when the money finally arrived, something strange had happened.

Around €150 had disappeared.

No warning.

No clear explanation.

How did the bank lose €150?” she asked later over coffee

The short answer: hidden banking fees.

Traditional banks often advertise “low transfer costs,” but the real charges are usually buried inside:

- exchange rate markups

- intermediary bank fees

- receiving bank deductions

Even in 2026 — despite modern fintech apps and faster payment systems — many people in France still lose significant money on international transfers simply because they use the wrong method.

And if you regularly send money abroad — to family, to another bank account, or even to buy property — those costs can add up quickly.

This guide was created to help expats in France avoid those mistakes.

Inside this article, you’ll learn:

- how international transfers actually work

- why traditional banks are often the most expensive option

- the best services for sending money abroad

- how to avoid hidden fees

- the safest way to transfer large amounts

- and the key rules you should know if you live in France

Whether you’re:

- sending money to family in Bangladesh or India

- transferring savings to the UK

- paying for property abroad

- or simply moving money between accounts

choosing the right transfer method can often save hundreds or even thousands of euros every year.

Before we explore the best services available today, it helps to understand why traditional bank transfers in France are often so expensive.

Why Traditional French Banks Are Often Expensive for International Transfers

If you walk into a branch of a major French bank like BNP Paribas or Société Générale, you’ll likely be greeted politely with a friendly “Bonjour.”

But behind that professional service, many international transfers still rely on banking systems that are decades old.

For expats sending money abroad, these systems can quietly increase costs especially when using traditional banks for international transfers.

Let’s look at the biggest ones.

1. Exchange Rate Markups (The Hidden Fee Most People Miss)

When most people send money internationally, they quickly check the exchange rate on Google.

That rate is called the mid-market exchange rate — the real exchange rate used by global financial markets.

Unfortunately, traditional banks rarely give customers that rate.

Instead, they usually add a markup, often between 3% and 5%.

Here’s a simple example.

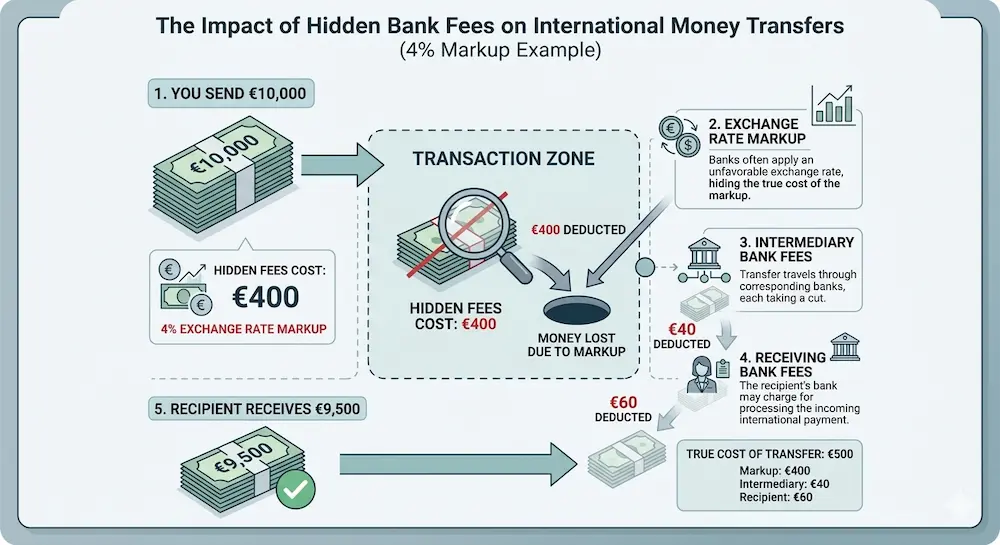

If you send €10,000 abroad and the bank adds a 4% exchange markup, you lose:

€400 immediately

And in many cases, this cost is not clearly visible on the receipt.

This hidden margin is often the largest cost of international transfers.

That’s why newer fintech platforms like Wise became extremely popular with expats — they use exchange rates that are much closer to the real market rate.

2. Multiple Banking Fees

On top of exchange rate markups, traditional banks may also charge several direct fees.

Typical international transfer fees include:

Emission Fee

This is the fee your bank charges just to send the transfer.

Typical range in France:

€15 – €30

Correspondent Bank Fees

When money moves across borders through the global banking network, it often passes through intermediary banks.

Each bank may deduct a small fee along the way.

The frustrating part?

You often don’t know these costs until the transfer arrives.

Receiving Bank Fees

Some banks also charge the recipient simply for receiving international funds.

These layered fees are why many expats are surprised when the final amount is smaller than expected.

3. Slow Transfer Infrastructure

Another issue with traditional banks is speed.

International bank transfers usually travel through the global banking network known as SWIFT.

The system is extremely secure, but it was originally developed in the 1970s.

Typical international bank transfer time:

• 1–3 business days (best case)

• 3–5 business days (common)

By comparison, many modern financial apps can process transfers within hours or even minutes.

4. The Digital Lag in Traditional Banking

Across Europe, banks are slowly adopting faster payment systems like SEPA Instant, which allows euro transfers within seconds.

The system is supported by regulators such as the European Central Bank.

However, many traditional banks have been slow to fully embrace these technologies.

Some banks still:

• limit instant transfer amounts

• hide the option inside their mobile apps

• or charge extra fees for faster transfers

As a result, many customers unknowingly choose slower and more expensive payment methods.

To understand how to avoid those costs, it helps to first understand how the French banking system handles payments.

The Technical Core: Understanding the French Banking System

For newcomers, French banking terminology can feel confusing at first.

You’ll often hear words like RIB, IBAN, BIC, SEPA, and SWIFT.

Once you understand these basics, sending or receiving international transfers becomes much easier.

The RIB: Your Financial Identity in France

In France, bank details are usually shared using a document called a RIB.

RIB stands for:

Relevé d’Identité Bancaire

Think of it as your financial identity card.

A RIB contains all the information someone needs to send money to your bank account.

Typical information on a RIB includes:

• account holder name

• IBAN

• BIC / SWIFT code

• bank name

• branch identifier

Unlike some countries where you only provide an account number, French payments often require the entire RIB document.

You will frequently need it for things like:

- receiving your salary

- paying rent

- setting up utility bills

- receiving reimbursements or refunds

If you live in France, you will probably send your RIB dozens of times every year.

IBAN vs BIC (SWIFT): What’s the Difference?

Two identifiers appear on every French bank account.

IBAN — International Bank Account Number

Your IBAN identifies your specific bank account.

French IBAN numbers always begin with:

FR

followed by 25 additional characters.

The structure usually looks like this:

FR + bank code + branch code + account number + checksum

A simple way to think about it:

Your IBAN is like the street address for your money.

BIC / SWIFT Code — Identifying the Bank

The BIC (also called a SWIFT code) identifies the bank itself, not your individual account.

For example, banks such as Crédit Agricole or BNP Paribas each have their own unique SWIFT code.

If the IBAN is the street address, the BIC is the postal sorting center that ensures the transfer reaches the correct bank.

Together, these two identifiers guide your transfer through the global banking system.

SEPA vs SWIFT: Choosing the Right Transfer Network

When sending money from France, your transfer usually travels through one of two payment networks.

Understanding the difference can help you avoid unnecessary fees.

SEPA (Single Euro Payments Area)

The SEPA system allows euro transfers across Europe.

It includes all EU countries plus several additional European states.

Advantages include:

• very low fees

• reliable transfers

• fast processing

With SEPA Instant, transfers can arrive in around 10 seconds.

SEPA is widely supported across Europe thanks to initiatives from institutions like the European Central Bank.

If you’re sending euros between countries like:

France

Germany

Spain

Italy

Netherlands

SEPA is almost always the cheapest and fastest option.

SWIFT (Global Transfers)

For transfers outside Europe, banks usually rely on the global network known as SWIFT.

This system enables transfers between banks worldwide.

However, SWIFT transfers often involve:

• higher fees

• slower processing times

• intermediary bank deductions

If you send money from France to countries such as:

United States

Bangladesh

India

Morocco

your transfer will typically move through the SWIFT network.

Because of this, choosing the right transfer provider becomes extremely important.

Best Ways to Send Money from France (2026 Comparison)

Once you understand how international transfers work in France, the next step is choosing the right transfer method.

Today, expats living in France generally use three main types of services to send money abroad:

1. Digital fintech platforms

2. Remittance specialists

3. Physical money transfer agencies

Each option is designed for slightly different situations. The best choice usually depends on:

- the destination country

- the transfer amount

- how the recipient wants to receive the money

Let’s explore the most common options used by expats in France.

1. Digital Transfer Platforms (Best for Most Expats)

For many people living in France, digital fintech apps are now the easiest and cheapest way to send money abroad.

Instead of visiting a physical shop or bank branch, you can complete the entire transfer from your phone.

Two platforms dominate the European market today:

- Wise

- Revolut

These services have become extremely popular among expats because they are:

• faster than traditional banks

• more transparent about fees

• often significantly cheaper

Wise — Transparent Exchange Rates

Among expats, Wise is often considered one of the most transparent international transfer platforms.

The key difference is simple.

Wise uses the mid-market exchange rate, which is the same rate you see on Google or financial websites.

Instead of hiding costs inside the exchange rate, Wise charges a small, clearly visible transfer fee.

When you send money, the app shows you:

• the real exchange rate

• the exact transfer fee

• the exact amount the recipient will receive

This transparency is one of the main reasons why Wise became so popular with international workers, freelancers, and expats.

Wise currently supports 50+ currencies, making it a practical solution for people sending money outside Europe.

Revolut — A Multi-Currency Banking App

Another extremely popular option in France is Revolut.

Unlike Wise, Revolut functions more like a full digital banking app.

Many expats use it for everyday banking as well as international transfers.

Some of its main advantages include:

• multi-currency accounts

• instant transfers between Revolut users

• a powerful mobile app

• spending analytics and budgeting tools

Revolut also offers competitive exchange rates during weekdays.

However, there are a few limitations to be aware of.

For example:

• weekend currency exchange often includes a small markup

• free currency exchange limits depend on your plan

Despite these limits, Revolut remains one of the most convenient financial apps for expats living in France.

2. Remittance Platforms (Best for Family Transfers)

If you regularly send money to family in countries like:

- Bangladesh

- India

- Philippines

- Morocco

remittance services are often designed specifically for these types of transfers.

Two well-known global providers include:

- Remitly

- WorldRemit

These companies focus on fast international remittances, often offering delivery methods such as:

• bank deposits

• mobile wallets

• cash pickup locations

In many countries, recipients can collect money from thousands of local agents such as grocery stores, pharmacies, or financial kiosks.

Transfers can often arrive within minutes or hours, depending on the delivery method.

However, because these services focus on convenience and speed, their exchange rate markup is sometimes slightly higher than fintech platforms like Wise.

3. Physical Money Transfer Shops (Very Popular in Paris)

Although digital apps are growing quickly, physical money transfer shops are still extremely popular, especially in large cities like Paris.

Many people prefer them because:

- they can send cash directly

- the process is simple

- recipients can collect cash quickly

Some of the most widely used services in France include:

- Western Union

- MoneyGram

- Ria Money Transfer

In Paris, these services are available in many locations such as:

• small financial service shops

• grocery stores

• phone shops

• travel agencies

Because of their massive global networks, recipients can often collect money from thousands of locations worldwide.

However, the downside is that fees and exchange rates can sometimes be higher than digital platforms.

These services are usually best when:

- the recipient needs cash pickup

- the sender prefers paying in cash

- or the recipient does not have a bank account

A Special Case: Sending Money to Bangladesh

For people sending money from France to Bangladesh, another platform has become extremely popular in recent years:

TapTap Send

Many expats in France use TapTap Send because it often offers very competitive exchange rates and promotions.

One important thing many users notice is that transfers to Bangladesh are sometimes free of transfer fees.

In other words:

You can send money without paying a visible transfer fee.

However, this can depend on:

- the destination country

- current promotions

- the payment method used

Even when the transfer fee is zero, it’s still worth checking the exchange rate, since part of the cost may be included there.

Still, for many Bangladeshi expats living in France, TapTap Send has become one of the most convenient ways to send money home.

How to Send Money from France (Step-by-Step Guide)

Once you’ve chosen a transfer platform for your transfer, the process is usually quite straightforward.

Most modern transfer services follow a similar process. If you’ve ever used an online banking app, the steps will feel very familiar.

Here’s what the typical process looks like.

Step 1: Verify Your Identity (KYC Process)

Before you can send money internationally, financial platforms must verify your identity.

This process is required by European financial regulations and helps prevent fraud, money laundering, and illegal transfers.

Most platforms — including services like Wise or Revolut — will ask for a few basic documents.

Typically, you may need to provide:

• passport or national ID

• residence permit (if applicable)

• proof of address in France

• sometimes a selfie verification

In France, proof of address is called a “Justificatif de Domicile.”

Accepted documents usually include:

• electricity bill

• internet bill

• rent receipt

• water bill

• tax document

In most cases, the document must be less than three months old.

The verification process usually takes only a few minutes, although sometimes it may take a few hours if the platform needs manual review.

Step 2: Add the Recipient (Beneficiary)

Next, you’ll need to add the person or account you want to send money to.

The exact details required depend on the destination country.

For example:

Inside Europe

You usually only need:

• IBAN

• recipient name

United Kingdom

• account number

• sort code

United States

• routing number

• account number

Many Asian or African countries

• bank name

• account number

• sometimes SWIFT/BIC code

Most apps allow you to save recipients, so you won’t need to enter the information again the next time you send money.

Step 3: Fund the Transfer

Once the recipient is added, the next step is funding the transfer.

Most services offer several payment methods:

• bank transfer

• debit card

• credit card

• sometimes Apple Pay or Google Pay

However, not all methods cost the same.

Bank transfers are usually the cheapest option, while card payments are often faster but slightly more expensive.

For example, if you fund a transfer on Wise using a debit card, the platform may charge a small processing fee.

If you instead send the money via bank transfer, the fee is usually lower.

Step 4: Confirm and Track the Transfer

After confirming the transfer, most platforms provide real-time tracking.

You can often see exactly where the money is during the transfer process.

Some apps even show stages such as:

• transfer initiated

• funds received by the platform

• currency conversion completed

• transfer sent to recipient bank

• funds delivered

It works almost like a package tracking system — but for your money.

Depending on the destination country and payment method, transfers can arrive anywhere between a few minutes and a few business days.

The Cheapest Way to Transfer Money from France

Even if you choose a good transfer platform, costs can still vary.

Many expats in France use a few simple strategies to reduce fees and avoid unnecessary costs.

Here are some of the most effective ones.

Use SEPA Transfers Whenever Possible

Inside Europe, the cheapest way to send money is usually through SEPA transfers.

SEPA stands for Single Euro Payments Area, a European payment system supported by institutions such as the European Central Bank.

The system allows euro transfers between European countries at very low cost.

Advantages include:

• extremely low fees

• reliable processing

• fast transfer times

With SEPA Instant, transfers can sometimes arrive in around 10 seconds, depending on the bank.

If you’re sending euros between countries such as:

France

Germany

Spain

Italy

Netherlands

SEPA transfers are almost always the cheapest and fastest option.

Avoid Card Payments When Possible

Many transfer apps allow you to fund a transfer using a debit or credit card.

While this is convenient, it is often more expensive.

Typical card processing fees range between:

0.5% – 2%

Instead, using a bank transfer to fund the transaction is usually cheaper.

For larger transfers, the difference can be significant.

For example:

Sending €5,000 using a card could cost €50–€100 more compared to a bank transfer.

Avoid Currency Conversion on Weekends

This is a small trick that many people don’t realize.

Foreign exchange markets operate 24 hours a day during weekdays, but they close on weekends.

Because of this, many financial apps add a weekend markup to protect themselves from sudden exchange rate changes.

For example, services like Revolut often add a small surcharge when currency conversion happens on Saturday or Sunday.

To avoid this extra cost:

Try converting currencies between Monday and Friday (CET) whenever possible.

Compare Services for Large Transfers

If you are transferring a large amount of money, it’s worth comparing several providers.

For transfers above €20,000 or €50,000, even a small difference in exchange rate can have a big impact.

Some people use foreign exchange brokers such as:

- OFX

- Currencies Direct

These companies specialize in large international transfers.

They often offer:

• better exchange rate margins

• dedicated account managers

• tools to lock in exchange rates

One feature offered by some FX brokers is called a forward contract, which allows you to lock today’s exchange rate for a transfer that will happen in the future.

For people buying property abroad or moving large savings between countries, this can help protect against currency fluctuations.

Sending Money from France to Countries Like Bangladesh, India, or Morocco

Many expats living in France regularly send money abroad to family members.

The best transfer method often depends on how the recipient receives the money.

In some countries, bank transfers are common. In others, people still prefer cash pickup services.

Understanding the local situation can help you choose the cheapest and fastest option.

Bank Account Transfers

If the recipient has a bank account, digital transfer platforms such as:

- Wise

- Revolut

usually provide the best exchange rates.

These platforms transfer money directly to the recipient’s bank account.

Advantages include:

• lower overall fees

• transparent exchange rates

• secure transfers

• easy tracking through the mobile app

For many expats sending money to countries such as India or Morocco, this method is often the most cost-effective.

Cash Pickup Transfers

In some regions, especially in parts of South Asia or Africa, recipients may prefer to receive cash instead of a bank transfer.

This is where global remittance services become useful.

Platforms such as:

- Western Union

- MoneyGram

- Ria Money Transfer

have huge global networks of agents.

Recipients can often collect cash from:

• grocery stores

• pharmacies

• exchange offices

• financial kiosks

In many cases, the transfer arrives within minutes.

However, the trade-off is that these services sometimes charge higher exchange rate margins compared to digital platforms.

Regulations and Transfer Limits in France

International money transfers are closely monitored by financial authorities to prevent fraud, tax evasion, and money laundering.

Banks and financial platforms in France operate under the supervision of regulators such as the Autorité de Contrôle Prudentiel et de Résolution.

Understanding these rules can help you avoid unexpected delays when sending money abroad.

The €10,000 Anti-Money Laundering Threshold

When large transfers occur, financial institutions must follow strict anti-money-laundering (AML) regulations.

If you send or receive a large amount — often around €10,000 or more — your bank or transfer platform may request additional documentation.

Examples of acceptable documents include:

• employment income records

• bank statements

• property sale documents

• inheritance documents

• gift declarations

This does not mean the transfer is illegal. It simply means the institution must verify the source of funds.

Most of the time, the process is quick if you can provide the required documents.

Declaring Foreign Financial Accounts

If you live in France and hold accounts with foreign financial institutions, you may need to declare them to the French tax administration.

This rule can apply to certain digital financial platforms as well.

The declaration is typically made when filing your annual tax return using Form 3916.

Failure to declare foreign accounts can result in penalties, so it is always wise to check your obligations with the French tax authorities or a tax professional.

Are Fintech Transfer Apps Safe?

Many people initially feel hesitant about using fintech apps instead of traditional banks.

However, most reputable transfer services operating in Europe are regulated as Payment Institutions or Electronic Money Institutions.

Companies such as:

- Wise

- Revolut

operate under European financial regulations.

They must follow strict rules that require customer funds to be safeguarded and separated from company operating funds.

This means that customer balances are protected even if the company experiences financial difficulties.

While no financial system is completely risk-free, reputable fintech platforms are generally considered safe and reliable for everyday international transfers.

Frequently Asked Questions

Is it legal to send money from France abroad?

Yes. Sending money internationally from France is completely legal.

However, financial institutions may request documentation for large transfers to comply with anti-money-laundering regulations.

How long does an international transfer take?

Transfer time depends on the payment network and the provider.

Typical timelines include:

SEPA transfers:

• seconds to one business day

SWIFT transfers:

• one to five business days

Digital fintech platforms often complete transfers faster than traditional banks.

Do I need to pay tax when transferring money abroad?

Simply transferring your own money usually does not trigger taxes.

However, tax implications may arise in certain situations, such as:

• transferring investment profits

• sending large financial gifts

• holding undeclared foreign accounts

If you are unsure, it is always wise to consult a qualified tax professional.

Final Thoughts: Choosing the Right Transfer Method

Sending money from France has become much easier over the past decade.

In the past, most people relied on traditional bank transfers or physical money transfer offices.

Today, expats have access to a wide range of options — from mobile fintech apps to global remittance networks.

For most people, digital platforms offer the best balance of cost, speed, and transparency.

However, the best choice always depends on your specific situation.

For example:

• digital platforms are often cheapest for bank-to-bank transfers

• cash pickup services remain useful in countries with limited banking access

• foreign exchange brokers may offer better rates for very large transfers

Taking a few minutes to compare services before sending money can often save hundreds of euros over time.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Always verify details with financial institutions or consult a qualified professional before making financial decisions.