Table of Contents

Understanding the French banking system helps expats manage daily finances smoothly.

Introduction: The First Step Toward Building Your Life in France

Banking in France as an expat can feel confusing at first, especially if you’re new to the system. Whether you’re a student, professional, or entrepreneur, understanding how banking works in France is essential for managing your daily life smoothly.

Moving to France is exciting. Whether you arrive as a student, a professional, an entrepreneur, or a retiree, the country offers an incredible lifestyle—beautiful cities, strong public services, and a vibrant culture built around food, community, and balance.

Choosing the right bank in France for expats will help you manage rent, salary, and daily expenses more smoothly.

But once the excitement of arriving settles down, most newcomers quickly discover something unexpected.

The French banking system can feel confusing at first.

Many expats assume that using their existing international bank card will be enough. In reality, daily life in France often requires a local bank account. You will likely need one to:

- receive a salary

- rent an apartment

- connect utilities

- receive healthcare reimbursements

- set up automatic payments

This is why having a reliable bank in France for expats is essential for everyday life.

When I first arrived in France, I remember sitting in a café filling out documents for an apartment rental. The landlord asked me to send something called a RIB. At that moment, I realized I had entered a financial system with its own terminology and rules.

At that moment, finding the right bank account in France as an expat became a priority.

Fast forward to 2026, and while banking in France has become much more digital, the basic structure of the system remains the same. Understanding a few key concepts early can save you a lot of time, stress, and money.

This guide is designed specifically for expats living in France. By the end, you will understand:

- how the French banking system works

- what IBAN, RIB, and BIC actually mean

- why a French bank account is often essential

- the differences between digital and traditional banks

- how to avoid unnecessary fees

Most importantly, you will learn how to build a simple and efficient banking setup for life in France.

1. Understanding the Basics of the French Banking System

Before opening a bank account in France, it helps to understand the key identifiers used across the European banking network. These identifiers are used in almost every financial transaction—from receiving your salary to paying your electricity bill.

The three most important terms you will encounter are:

- IBAN

- RIB

- BIC / SWIFT

Once you understand how these work, the rest of the French banking system becomes much easier to navigate.

The IBAN: Your Main Banking Identity in Europe

The IBAN (International Bank Account Number) is the standard account identifier used across Europe and many other countries.

Every bank account within the SEPA (Single Euro Payments Area) has a unique IBAN.

A French IBAN usually begins with:

FR + 25 additional characters

Example format:

FR76 XXXX XXXX XXXX XXXX XXXX XXX

The IBAN is used for almost every financial transaction in France, including:

- receiving your salary

- paying rent

- sending bank transfers (called virements)

- receiving government reimbursements

- setting up automatic payments

The European Union introduced IBAN to simplify cross-border payments across Europe.

According to the European Commission’s SEPA rules:

All euro transfers within SEPA must use the IBAN as the primary account identifier.

Although European regulations prohibit IBAN discrimination, some French companies still prefer accounts with a French IBAN for administrative reasons. For this reason, many expats eventually open a French bank account even if they already use international fintech services.

The RIB: A Classic Feature of French Banking

One term that surprises many newcomers is RIB, which stands for:

Relevé d’Identité Bancaire

A RIB is simply a document containing your bank account details. Think of it as a banking identity card.

A typical RIB includes:

- your name

- your IBAN

- your BIC code

- your bank’s identification details

In the past, banks would mail a printed RIB booklet to customers. Today, things are much simpler. Almost every bank allows you to download your RIB as a PDF from the mobile banking app.

You will likely send your RIB many times in France when setting up services such as:

- renting an apartment

- connecting electricity or internet

- registering insurance

- receiving salary payments

Because of this, it is useful to keep a digital copy of your RIB saved on your phone or email.

The concept of the RIB is specific to the French banking culture, but it remains a standard document used by businesses and institutions across the country.

BIC / SWIFT Code: Mostly Used for International Transfers

The BIC (Bank Identifier Code)—also known as the SWIFT code—identifies a specific bank internationally.

While the IBAN identifies your account, the BIC identifies the bank itself.

You will usually need a BIC when:

- receiving money from outside Europe

- sending funds internationally

- receiving international business payments

For most payments inside Europe, the IBAN alone is usually enough.

Since the introduction of SEPA, many domestic transfers in the euro area no longer require the BIC at all.

More information about international bank codes can be found on the SWIFT network website.

2. Why You Need a Bank in France for Expats

Many newcomers initially assume they can continue using their existing international bank card after moving to France.

For short visits, this may work. But if you plan to live in France for several months or longer, having a local bank account quickly becomes essential.

French administrative systems often rely heavily on bank accounts for payments, reimbursements, and automated billing.

Here are some of the most common situations where a French account becomes necessary.

Receiving Your Salary

Many employers in France prefer paying salaries directly into French bank accounts.

While European regulations technically allow payments to any SEPA account, some payroll systems are designed primarily for domestic IBANs.

Providing a French IBAN often makes administrative processes faster and smoother.

Healthcare Reimbursements

France has one of the strongest public healthcare systems in Europe.

When you register with the national health insurance system (Assurance Maladie), reimbursements for medical expenses are usually transferred directly to your bank account.

To receive these reimbursements, you must connect your bank account to your health profile.

For more official information about healthcare reimbursements can be found there website.

Renting an Apartment

Renting accommodation in France almost always requires bank information.

Landlords or rental agencies often request a RIB for:

- monthly rent payments

- security deposits

- automatic transfers

Without a French account, renting long-term accommodation can become more complicated.

Utilities and Automatic Payments

Many essential services in France rely on automatic bank debit, called:

Prélèvement automatique

This system allows companies to withdraw payments automatically from your account each month.

It is commonly used for:

- electricity

- internet

- mobile phone plans

- insurance

- subscriptions

Automatic debit is one of the most common payment systems in France, which is why having a compatible bank account is important.

Cheques Are Still Used in France

While many countries have almost completely abandoned cheques, France still uses them more frequently than expected.

Many traditional banks still provide cheque books (chéquiers).

Cheques may still be used for:

- school activities

- local associations

- security deposits

- certain service payments

Although their usage is gradually declining, cheques remain part of everyday financial life in France.

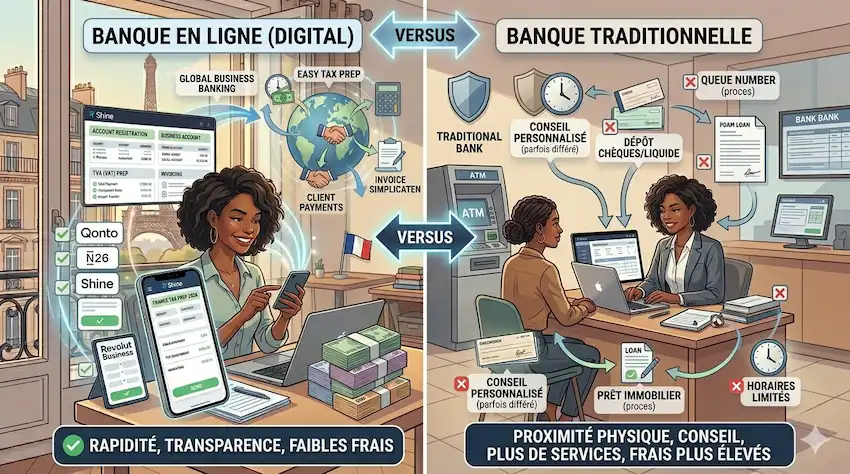

3.Best Bank in France for Expats: Digital vs Traditional

In 2026, expats living in France generally choose between two main types of banks.

Choosing the right banking option in France depends on your financial needs and lifestyle.

Each option has advantages depending on your financial needs.

Digital Banks (Neobanks)

Digital banks operate almost entirely online through mobile apps and websites.

They have grown rapidly across Europe in the last decade and are often the fastest way for newcomers to open an account.

Typical advantages include:

- quick online account setup

- low or zero monthly fees

- modern mobile banking apps

- English-language support

Because these banks operate digitally, the account opening process can sometimes be completed in less than a day.

For many newcomers, a digital bank account in France is the fastest way to get started.

However, digital banks also have limitations.

Some services may be restricted, including:

- depositing cash

- depositing cheques

- applying for mortgages

- complex financial services

For everyday spending and international transfers, however, many expats find digital banks extremely convenient.

Traditional French Banks

Traditional banks still play a major role in the French financial system.

These banks usually have physical branches where customers can speak with a financial advisor.

Common advantages include:

- in-person customer service

- easier access to loans and mortgages

- support for more complex financial situations

- access to cheque services and cash deposits

However, traditional banks may also involve:

- higher monthly account fees

- longer account opening procedures

- more paperwork

A traditional bank in France for expats is often better for long-term financial needs like loans and mortgages.

For many expats, the most practical strategy is to combine both systems—using a digital bank for daily spending while maintaining a traditional bank relationship for long-term financial needs.

4. Types of Banks in France: Digital Banks vs Traditional Banks

Choosing the right bank is one of the most important financial decisions when living in France.

The country offers a wide range of banking options, from large traditional institutions with hundreds of branches to fully digital banks that operate entirely through mobile apps.

Each option has its own advantages depending on your situation. Some banks are better for mortgages and long-term financial relationships, while others are designed for low-cost everyday banking.

Here are some of the most popular banks used by expats in France.

Traditional French Banks

Traditional banks are still the backbone of the French financial system. They typically provide physical branches, dedicated advisors, and access to services like mortgages or business loans.

Some of the most well-known institutions include:

- BNP Paribas

- Société Générale

- Crédit Agricole

These banks offer a wide range of services such as:

- personal accounts

- business banking

- loans and mortgages

- savings accounts

- investment products

Because they have physical branches, they can be especially helpful when dealing with more complex financial matters or administrative procedures.

However, traditional banks often involve:

- monthly account maintenance fees

- appointment-based account opening

- more paperwork for expats

Official information about French banking institutions and regulations can be found through the French central bank.

Digital Banks (Online Banks)

In recent years, digital banks have become extremely popular among expats because they are faster to open and often cheaper to use.

Some widely used online banks in France include:

- Hello bank!

- Bourso Banque

Digital banks typically offer:

- very low monthly fees

- quick account opening

- strong mobile banking apps

- easy international payments

Because they operate primarily online, they usually require less paperwork and fewer in-person appointments.

For many expats, digital banks are often the fastest way to get a French IBAN after arriving in the country.

International Fintech Services Used by Expats

Many expats also use global fintech services alongside a French bank account.

Popular examples include:

- Wise

- Revolut

- N26

These services are particularly useful for:

- international transfers

- multi-currency accounts

- travel spending

- lower foreign exchange fees

However, they may not always replace a traditional French bank account for administrative purposes.

5. How to Open a Bank in France for Expats (Step-by-Step Guide)

Understanding how to open a bank account in France early can save you weeks of stress. Many expats encounter a frustrating situation shortly after arriving in France.

You may need a French address to open a bank account, but at the same time you may need a bank account to rent an apartment.

Starting with a digital bank in France for expats is often the easiest way to break this catch-22.

This circular problem is surprisingly common and often referred to as the expat banking catch-22.

Fortunately, there are practical ways to solve it.

Step 1: Start With a Digital Bank

Digital banks are often the easiest starting point for newcomers because their registration process can usually be completed online.

Most digital banks require:

- a passport or ID

- a selfie verification

- a temporary address

Once approved, you will receive an IBAN and debit card, allowing you to begin managing daily expenses.

Step 2: Use Temporary Proof of Address

If you are staying temporarily with friends or family, you may still be able to open an account using an attestation d’hébergement.

This document confirms that someone is hosting you at their address.

Other acceptable documents may include:

- temporary rental agreements

- work contracts

- university enrollment documents

Step 3: Upgrade Later if Needed

Once you have settled in France and secured long-term housing, you may decide to open a traditional bank account.

Some expats maintain two accounts:

- a digital bank for everyday spending

- a traditional bank for long-term financial services

This hybrid strategy provides flexibility while keeping banking costs relatively low.

6. Documents Required to Open a Bank Account in France

To open a bank account in France as an expat, you’ll need a few key documents that verify identity and residency.While requirements vary slightly between banks, most institutions request the same core information.

Typical documents include:

Identification

Banks must verify your identity as part of European anti-money-laundering regulations.

Acceptable documents usually include:

- passport

- national identity card

- residence permit (if applicable)

Proof of Address

Banks also require proof that you live in France.

- Common examples include:

- utility bills

- rental contracts

- tax documents

an attestation d’hébergement from your host

Proof of Income or Activity

Some banks may request information about your professional activity.

This might include:

- employment contract

- student certificate

- business registration documents

These checks are part of Know Your Customer (KYC) regulations designed to prevent financial fraud.

More details about banking consumer rights and procedures are available through the French government’s financial information service.

7. Hidden Fees to Watch Out For

When choosing a bank account in France, it’s important to watch for hidden fees that can surprise you.

Even with careful planning, newcomers sometimes get caught by unexpected banking costs. Banks may include extra services automatically or offer “premium” packages that you might not need.

Common Hidden Fees

- Account maintenance fees (frais de tenue de compte) – Monthly fee for keeping your account active

- Card fees – Some banks charge annual fees for debit or credit cards

- Overdraft fees (frais d’incident de paiement) – If you overdraw your account

- International transfer fees – Standard bank transfers abroad may be expensive

Tip: Always request a full fee breakdown from your bank before signing up. Ask specifically about monthly fees, withdrawal charges, and foreign transfer costs.

The Livret A: France’s Most Popular Savings Account

One of the best financial tools in France for residents is the Livret A. It is a government-regulated savings account that offers several advantages:

- Tax-free interest – No income tax or social contributions on earnings

- High security – Government-backed deposits

- Easy withdrawals – Funds are accessible anytime

Deposit limit: Approximately €22,950 per individual

Many residents use the Livret A as an emergency fund, separate from their main checking account.

8. International Money Transfers for Expats

Expats frequently need to send or receive money internationally. While traditional banks can do this, they often charge higher fees and offer less favorable exchange rates.

Popular Alternatives

- Wise (formerly TransferWise) – low-cost international transfers with real exchange rates

- Revolut – multi-currency accounts and instant transfers

- Western Union / MoneyGram – convenient cash pickup options

For regular transfers, using specialized fintech services often saves money and reduces delays compared to standard bank transfers.

9. Essential French Banking Vocabulary

Learning a few key terms can make life much easier when dealing with banks in France. Even if you open a bank in France for expats, knowing these terms will prevent mistakes and delays.

Here are some of the most common ones:

- Virement = Bank transfer

- Prélèvement = Automatic debit

- Solde = Account balance

- Frais = Fees

- Chéquier = Cheque book

- Faire opposition = Block a bank card

Even a basic familiarity with these words can help avoid misunderstandings and delays in banking operations.

10. Common Banking Problems for Expats

When setting up a bank account in France, expats may encounter a few common challenges:

- Account rejection – Some banks may require extra documents if you are not an EU citizen

- American expats and FATCA – Banks are required to report US citizens’ accounts to the IRS. Some smaller banks may decline American customers

- The catch-22 of address proof – Needing a bank account to rent an apartment but needing a rental contract to open the account

- Language barriers – While many banks offer English support, smaller branches may not

Tip: Start with a digital bank to get a working IBAN, then upgrade to a traditional bank for more complex needs.

11. FAQs

Q: What is the best bank in France for expats?

A: It depends on your needs—digital banks for quick setup, traditional banks for long-term services, and fintech tools for international transfers.

Q: Can I open a French bank account before arriving?

A: Some digital banks allow online registration before arrival. Traditional banks usually require a physical visit.

Q: What is “Droit au Compte”?

A: If several banks refuse to open an account, French law guarantees the right to a basic bank account. The national banking authority can require a bank to open one.

Q: Are checks still commonly used?

A: Yes, especially for rental deposits, school payments, and local services. But digital payments are increasingly popular.

Q: Do I need a French address to open an account?

A: Usually yes, but temporary proof like attestation d’hébergement may work for initial account opening.

12. Summary: A Smart Banking Strategy for Expats

Securing the right banking setup in France is the first step toward stress-free financial management.

Managing your finances in France is easier if you combine multiple tools:

1. Digital bank for everyday spending – Quick, low-cost, English-friendly

2. Traditional bank for long-term needs – Mortgages, cheques, and personal financial advice

3. Specialized fintech for international transfers – Lower fees and better exchange rates

Key Takeaways:

Secure your IBAN

Keep a copy of your RIB

Understand automatic payments (prélèvement)

Be aware of hidden fees

Consider a Livret A for emergency savings

Once your accounts are set up, banking becomes routine, and you can focus on enjoying life in France—whether it’s sipping coffee in a Parisian café or exploring the French countryside.

Disclaimer: This guide is for informational purposes only. Banking policies, fees, and regulations may change. Always verify details with your bank or a licensed financial advisor.